Choosing where to spend your retirement years is one of the most consequential decisions you’ll ever make.

It touches everything: your finances, your health, your social life, and your daily sense of purpose.

The right city can stretch a modest pension into a comfortable lifestyle, while the wrong one can drain savings faster than you’d expect.

With shifting global economics, evolving visa programs, and new healthcare data available in 2026, the calculus has changed significantly from even a few years ago. This guide breaks down five cities across four continents that offer retirees a genuine shot at a fulfilling, affordable, and healthy next chapter.

Article Highlights:

- The five cities span Europe, Central America, South America, and Southeast Asia, each offering distinct advantages for different retirement priorities.

- Affordability analysis includes real 2026 cost-of-living data, with particular attention to retirees living primarily on Social Security income.

- Healthcare access is evaluated city by city, factoring in both public systems and private options available to foreign residents.

- Practical logistics like visa pathways, international payment management, and quality-of-life scoring are covered to help you move from dreaming to doing.

Defining the 2026 Retirement Landscape

The global retirement picture in 2026 looks fundamentally different from a decade ago.

Inflation across much of the developed world has cooled from its 2022-2023 peaks, but the cumulative price increases left their mark.

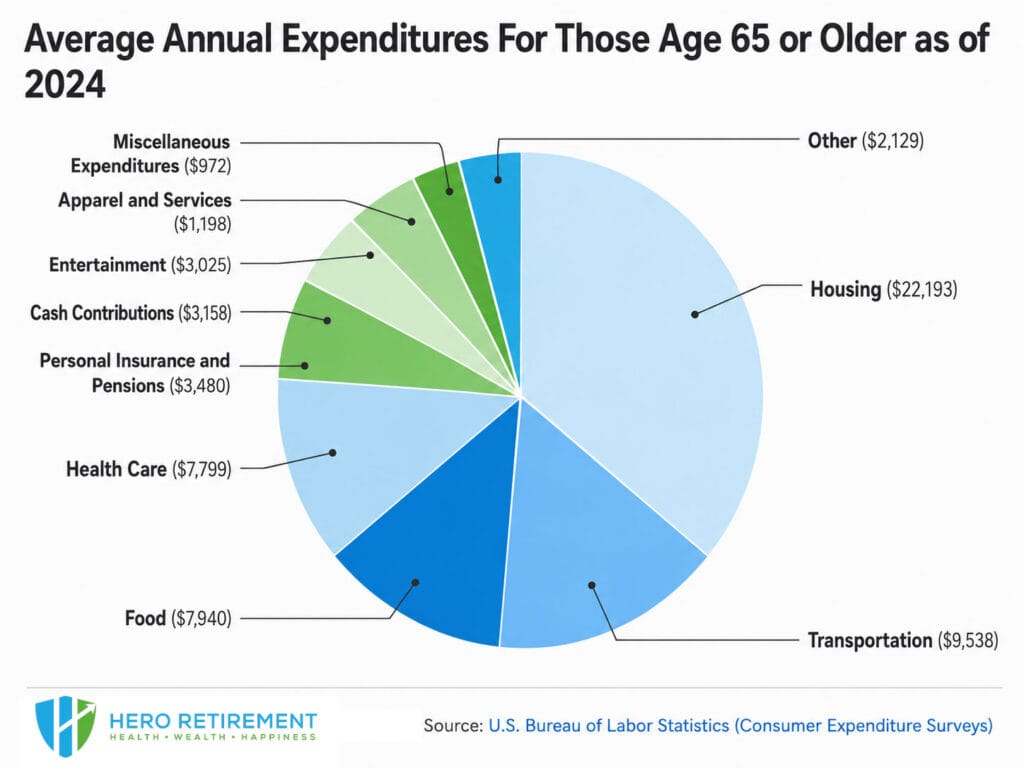

In the United States, the average retired couple now needs roughly $5,120 per month, according to the Bureau of Labor Statistics’ latest Consumer Expenditure Survey. That figure climbs sharply in major metro areas like New York, San Francisco, and Miami, where housing alone can consume 40-50% of a retiree’s budget.

This reality is pushing more Americans, Canadians, and Europeans to consider international retirement destinations.

The number of U.S. retirees receiving Social Security payments abroad grew by 8.3% between 2023 and 2025, per Social Security Administration data. That trend shows no signs of slowing.

The appeal is straightforward: geo-arbitrage lets you maintain or improve your standard of living by relocating to a place where your dollars, euros, or pounds go further.

But cost savings alone don’t make a great retirement destination…

You need reliable healthcare, a stable political environment, reasonable safety, cultural richness, and a welcoming expat community. The five cities in this guide were selected because they score well across all of these dimensions, not just one or two.

Economic Trends and the Quality of Life Index for 2026 Relocation

Several economic shifts in 2026 are reshaping where retirees can live well.

The U.S. dollar has strengthened modestly against several emerging-market currencies, making destinations in Latin America and Southeast Asia even more attractive for dollar-denominated income.

Meanwhile, the eurozone’s economic recovery has stabilized property markets in Southern Europe, creating opportunities for retirees who want European culture without Northern European price tags.

The Mercer Quality of Living Index and the InterNations Expat Insider Survey are two very well known publications. Cities in Portugal, Spain, Malaysia, Costa Rica, and Ecuador all recently climbed in categories that matter most to retirees: personal safety, healthcare access, ease of settling in, and overall satisfaction.

One underappreciated trend is the rise of “retirement visa” competition among countries.

Nations are actively courting retirees because they bring stable foreign income without competing for local jobs. Portugal, Malaysia, and Ecuador have all updated or expanded their retirement visa programs in the past two years, making the bureaucratic path smoother than it was even in 2024.

Currency risk remains a real consideration.

If you’re drawing Social Security or a U.S. pension, a sudden dollar weakening could erode your purchasing power abroad.

Hedging strategies, like maintaining accounts in both your home currency and your destination currency, can help. Some retirees keep 12-18 months of living expenses in local currency to buffer against exchange rate swings.

Prioritizing Best Healthcare Systems for Senior Citizens by City

Healthcare is the non-negotiable factor.

You can tolerate a smaller apartment or fewer restaurant meals, but you can’t compromise on medical care as you age. The best healthcare systems for senior citizens vary by city, and the gap between good and inadequate can be enormous.

When evaluating healthcare for retirement abroad, consider five dimensions: proximity to quality hospitals, availability of English-speaking doctors, cost of private insurance for foreign residents, prescription drug pricing, and emergency response infrastructure.

A city might have excellent hospitals in its center but poor ambulance response times in outlying neighborhoods where expats often settle.

The World Health Organization’s 2025 Global Health Observatory data shows that all five cities in this guide have hospitals rated in the top tier for their respective regions. Private health insurance for a 65-year-old in these destinations typically ranges from $80 to $350 per month, a fraction of what comparable coverage costs in the U.S. without Medicare.

One critical note: Medicare does not cover you outside the United States.

If you retire abroad before age 65, you’ll need to bridge the gap entirely with private coverage. Even after 65, you’ll rely on local insurance or out-of-pocket payments. This is a planning detail that trips up many aspiring expat retirees, so build it into your budget from day one.

Lisbon, Portugal: The Premier European Choice

Lisbon consistently ranks among the top cities for retirees choosing Europe.

The Portuguese capital combines Old World charm with a surprisingly modern infrastructure, a thriving food scene, and one of the continent’s most welcoming attitudes toward foreign residents. The city’s mild climate, with average winter temperatures around 12°C (54°F) and warm but not brutal summers, suits retirees who want four seasons without extreme weather.

The cost of living in Lisbon has risen over the past five years, driven partly by its popularity among digital nomads and retirees. Still, it remains significantly cheaper than Paris, London, or Amsterdam.

A retired couple can live comfortably on $2,500 to $3,200 per month, including rent for a one- or two-bedroom apartment in a central neighborhood like Graça or Alfama. Groceries, public transit, and dining out are all 30-40% cheaper than comparable U.S. cities.

Lisbon’s cultural offerings are rich and accessible.

Free or low-cost museums, live fado music, neighborhood festivals, and easy day trips to Sintra, Cascais, and the Alentejo wine region fill your calendar without straining your budget. The city’s walkability varies by neighborhood, as those famous hills are beautiful but challenging for anyone with mobility concerns. The metro system, trams, and buses provide solid alternatives.

The expat community in Lisbon is large and well-organized.

English is widely spoken, especially among younger Portuguese, and you’ll find expat meetup groups, international churches, and English-language social clubs throughout the city. Loneliness, one of the biggest risks in retirement relocation, is easier to combat here than in more isolated destinations.

Navigating the D7 Visa and Tax Incentives

Portugal’s D7 Passive Income Visa is the primary pathway for retirees.

It’s designed for people who can demonstrate a stable income from pensions, Social Security, investments, or rental properties.

The minimum income requirement in 2026 is approximately €870 per month for the primary applicant, with additional amounts for spouses and dependents. That threshold is well within reach for most Social Security recipients.

The application process involves gathering documents including proof of income, a clean criminal record, health insurance coverage valid in Portugal, and proof of accommodation.

Processing times vary, but most applicants receive approval within two to four months.

The initial visa grants a one-year residency, renewable for successive two-year periods. After five years, you’re eligible for permanent residency or Portuguese citizenship.

Portugal’s Non-Habitual Resident (NHR) tax regime was a major draw for years, offering a flat 10% tax rate on foreign pension income.

The program was officially closed to new applicants in 2024, but a modified successor scheme introduced in 2025 still offers tax advantages for retirees. Under the current rules, foreign pension income is taxed at a reduced rate of 10% for the first ten years of residency, though the specific conditions have tightened. Consult a Portuguese tax advisor before making assumptions about your tax liability.

One practical tip: open a Portuguese bank account as early as possible in the process.

You’ll need it for rent payments, utility bills, and proving financial ties to the country during visa renewals. NIF, your Portuguese tax identification number, is the first thing to obtain, and you can get one even before arriving in the country through a fiscal representative.

San José, Costa Rica: Sustainable Living and Longevity

Costa Rica has attracted retirees for decades.

San José remains the hub for those who want access to urban amenities while living in one of the world’s most biodiverse countries. The capital city sits in the Central Valley at about 1,100 meters elevation, giving it a spring-like climate year-round. Daytime temperatures hover around 24°C (75°F), and you won’t need air conditioning or heavy heating.

The country’s commitment to environmental sustainability isn’t just marketing…

Costa Rica generated over 98% of its electricity from renewable sources in 2025, and the government’s decarbonization plan is among the most ambitious in the Americas. For retirees who care about living in alignment with environmental values, this matters.

San José itself is a mid-sized city with a metropolitan population of about 2.2 million.

It’s not a beach town, and it won’t win beauty contests against Lisbon or Valencia. But what it offers instead is practicality: international flights through Juan Santamaría Airport, a wide range of shopping and dining, and proximity to both Pacific and Caribbean coasts within a few hours’ drive.

Many retirees use San José as a base and take regular trips to beach towns like Manuel Antonio or Tamarindo.

The cost of living for a retired couple runs between $2,000 and $2,800 per month, depending on lifestyle.

Rent in the San José metro area is reasonable, with two-bedroom apartments in desirable neighborhoods like Escazú or Santa Ana ranging from $800 to $1,400 per month. Fresh produce at local ferias (farmers’ markets) is both excellent and cheap.

The Caja System and Private Healthcare Excellence

Costa Rica’s public healthcare system, known as the Caja Costarricense de Seguro Social (CCSS or simply “la Caja”), is available to all legal residents.

As a retiree with legal residency, you’ll pay a monthly contribution based on your reported income, typically around 7-11% of your pension. This gives you access to the entire public system, including hospital care, specialist visits, and prescription medications.

The Caja system is good but not fast. Wait times for specialist appointments and elective procedures can stretch weeks or months.

Many expat retirees supplement their Caja coverage with private insurance, which costs between $100 and $300 per month depending on age and coverage level. Private hospitals in San José, including CIMA Hospital and Clínica Bíblica, are accredited by the Joint Commission International and offer care comparable to top U.S. facilities at a fraction of the cost.

A hip replacement in San José’s private system, for example, typically costs $12,000 to $18,000, compared to $40,000 or more in the United States. Dental care is similarly affordable, and Costa Rica has become a destination for medical tourism partly because of this price differential.

Costa Rica’s Pensionado visa requires proof of at least $1,000 per month in pension income.

The application process takes three to six months and requires an FBI background check, authenticated pension statements, and a Costa Rican consulate appointment. Once approved, you receive a two-year residency that’s renewable, and after three years, you can apply for permanent residency.

Cuenca, Ecuador: Most Affordable Places for Retirees on Social Security

If your primary concern is stretching a fixed income as far as possible, Cuenca deserves serious attention.

This highland city of roughly 400,000 people sits at 2,500 meters in Ecuador’s southern Andes, and it’s become one of the most affordable places for retirees on Social Security anywhere in the Western Hemisphere.

The average retired couple here can live well on $1,500 to $2,200 per month, including rent, food, healthcare, and entertainment.

Cuenca’s historic center is a UNESCO World Heritage Site, filled with colonial architecture, cobblestone streets, flower markets, and a lively arts scene. The city has a European feel that surprises first-time visitors.

Four rivers run through the urban area, lined with parks and walking paths. The climate is mild and consistent: expect daytime highs around 18-21°C (65-70°F) year-round, with cool evenings.

Ecuador uses the U.S. dollar as its official currency, which eliminates exchange rate risk entirely for American retirees.

Your Social Security check arrives in dollars, you spend in dollars, and you never worry about currency fluctuations eating into your purchasing power. This single factor makes Cuenca uniquely attractive among international retirement destinations.

The expat community in Cuenca is substantial, with an estimated 5,000-8,000 foreign retirees living in the city.

You’ll find English-language newspapers, expat social clubs, volunteer organizations, and even American-style restaurants. But the city hasn’t lost its Ecuadorian character. Local markets, traditional festivals, and Spanish-language daily life remain the dominant culture, which is exactly what many retirees want.

Living Well on a Fixed Budget in the Andes

The numbers in Cuenca are striking.

A comfortable two-bedroom apartment in a good neighborhood like El Vergel or Yanuncay rents for $450 to $700 per month. A full lunch at a local almuerzo restaurant costs $2.50 to $3.50. A monthly bus pass is under $15. A visit to a general practitioner runs $20 to $35 out of pocket.

Ecuador offers retirees over 65 a range of discounts mandated by law.

You’ll receive 50% off domestic airfare, up to 50% off utility bills, and discounts on property taxes and public transportation. These senior benefits are codified in the constitution and apply to all legal residents, not just citizens.

The Pensioner Visa (Visa de Jubilado) requires proof of pension or Social Security income of at least $1,450 per month in 2026.

The application process involves apostilled documents, a background check, and an appointment at an Ecuadorian consulate or immigration office. Processing typically takes one to three months. The visa is initially valid for two years and is renewable indefinitely.

Healthcare in Cuenca is affordable but requires some planning.

The public IESS system is available to residents who contribute, and private insurance through companies like BMI or Humana Ecuador costs $100 to $200 per month for comprehensive coverage. Hospital Universitario del Río and Hospital Monte Sinaí are the top private facilities. For complex procedures, some retirees travel to Quito or even back to the U.S., but routine care and even moderately complex treatments are handled well locally.

One honest caveat: Cuenca’s altitude affects some people.

At 2,500 meters, you may experience mild altitude symptoms during your first week or two, and people with certain respiratory or cardiac conditions should consult their doctor before committing. Most healthy retirees adjust quickly, but it’s worth a trial visit of at least a month before selling your house and shipping your belongings.

George Town, Malaysia: Modern Infrastructure Meets Tradition

George Town, the capital of Penang state, offers something none of the other cities on this list can match: a genuine fusion of Malay, Chinese, Indian, and European cultures.

This UNESCO-listed city on Malaysia’s northwest coast has become a magnet for retirees from Australia, the UK, Japan, and increasingly the United States.

The cost of living in George Town is remarkably low for what you get.

A retired couple can live comfortably on $1,800 to $2,600 per month. Modern condominiums with pools and gyms rent for $500 to $900 per month. The food scene alone is worth the move: George Town is regularly cited as one of the best street food cities on the planet, and a hawker center meal costs $1.50 to $3.00.

Malaysia’s MM2H (Malaysia My Second Home) visa program was revamped in 2024 and further adjusted in early 2026.

The current tier system offers a “Silver” category for applicants over 50, with reduced financial requirements compared to younger applicants.

You’ll need to show a minimum monthly offshore income of RM5,000 (approximately $1,100 USD) and maintain a fixed deposit of RM150,000 ($33,000 USD) in a Malaysian bank. These thresholds are accessible for most retirees with a combination of Social Security and modest savings.

George Town’s infrastructure is excellent by Southeast Asian standards.

The Penang International Airport connects to Kuala Lumpur, Singapore, Bangkok, and other regional hubs. Roads are well-maintained, and the Rapid Penang bus system covers the island effectively. Internet speeds are fast and reliable, which matters if you plan to stay connected with family back home through video calls.

World-Class Medical Tourism for Expats

Malaysia’s healthcare system is one of the strongest in Asia. Penang specifically has developed into a major medical tourism hub. Penang Adventist Hospital, Gleneagles Penang, and Loh Guan Lye Specialists Centre all provide care that rivals hospitals in Singapore or Hong Kong at significantly lower prices.

A comprehensive health screening that might cost $2,000 in the U.S. runs about $200-$400 in Penang.

Cardiac bypass surgery averages $9,000 to $12,000, compared to $70,000 or more stateside. Private health insurance for a 65-year-old expat costs approximately $150 to $300 per month with good coverage, including hospitalization and specialist care.

English is widely spoken in Malaysian hospitals, particularly in Penang, where the medical tourism industry has driven English-language proficiency among healthcare workers.

You won’t struggle to communicate with your doctor, and medical records are typically maintained in English.

The public healthcare system is also available to residents at minimal cost, though most expat retirees prefer private facilities for shorter wait times and more comfortable accommodations. Malaysia’s dual public-private system gives you flexibility that few other countries in this price range can offer.

One consideration specific to Malaysia: the tropical climate.

George Town is hot and humid year-round, with temperatures typically between 27-33°C (80-91°F). If you thrive in warm weather, you’ll love it. If you prefer temperate climates, the adjustment can be significant. Many retirees cope by choosing air-conditioned condos and scheduling outdoor activities for early morning or evening hours.

Valencia, Spain: The Ultimate Balance of Culture and Safety

Valencia rounds out this list of top retirement cities for 2026… and it might be the most well-rounded option of the five.

Spain’s third-largest city offers Mediterranean climate, world-class cuisine, excellent public healthcare, rich cultural life, and a cost of living that’s 30-40% lower than Barcelona or Madrid. It’s the city that checks the most boxes simultaneously.

The average retired couple can live well in Valencia on $2,400 to $3,200 per month.

Rent for a two-bedroom apartment in neighborhoods like Ruzafa, Benimaclet, or El Cabanyal ranges from $700 to $1,100 per month. Groceries from the Mercado Central, one of Europe’s oldest continuously operating food markets, are fresh and affordable. A glass of excellent local wine at a neighborhood bar costs $2 to $3.

Valencia’s climate is a major draw.

The city averages over 300 sunny days per year, with mild winters (average January temperature of 11°C/52°F) and warm summers moderated by sea breezes. The beach is a short bus or bike ride from the city center, and the Turia Gardens, a nine-kilometer park built in a former riverbed, provides green space that winds through the entire city.

Spain’s Non-Lucrative Visa is the standard pathway for retirees.

You’ll need to demonstrate sufficient financial means, typically around €2,400 per month for a single applicant or €3,000 for a couple, along with private health insurance and a clean criminal record. The visa grants a one-year residency, renewable for two-year periods, with a path to permanent residency after five years.

Safety is another strong point.

Valencia regularly ranks among the safest large cities in Europe, with low violent crime rates and a general sense of security that lets you walk home at night without anxiety. The Global Peace Index and Numbeo’s crime data both support this reputation.

Walkability and Public Transit Integration

One of Valencia’s standout qualities for retirees is how easy it is to live without a car.

The city’s flat terrain makes walking and cycling practical for most people, including those with moderate mobility limitations. The municipal bike-sharing program, Valenbisi, costs about €30 per year and has stations throughout the city.

The metro system covers the urban area and extends to nearby towns and beaches.

A senior transit pass (Bono Oro) for residents over 65 costs just €10 per month and provides unlimited travel on metro, bus, and tram. This kind of affordable, comprehensive public transit is rare and incredibly valuable for retirees who want independence without the expense and hassle of car ownership.

Valencia’s neighborhoods are designed around the concept of the “15-minute city,” where daily necessities like groceries, pharmacies, cafes, and medical clinics are within a short walk. This isn’t a planning buzzword here; it’s how the city actually functions. You’ll find a farmacia, a bakery, and a produce shop within a few blocks of almost any residential area.

Spain’s public healthcare system, the Sistema Nacional de Salud, is available to legal residents and is consistently ranked among the best in Europe by the WHO.

Hospital La Fe and Hospital Clínico Universitario are both major teaching hospitals with strong reputations. Private insurance, if you prefer it, costs $150 to $250 per month and gives you access to shorter wait times and private room options.

The social dimension of life in Valencia deserves mention too.

Spanish culture is inherently social, built around shared meals, neighborhood bars, and public gathering spaces.

Retirees who engage with local life, even with basic Spanish, often report a stronger sense of community than they experienced in their home countries. Language classes are widely available and affordable, and many Valencians are patient and encouraging with learners.

Essential Preparation for Your 2026 Move

Picking a city is the exciting part.

The practical preparation is where many aspiring expat retirees stall out. Moving abroad in retirement involves legal, financial, medical, and emotional planning that can take six to twelve months to complete properly. Rushing this process leads to costly mistakes and unnecessary stress.

Start with a scouting trip.

Spend at least two to four weeks in your target city, and don’t stay in tourist areas. Rent an apartment in a residential neighborhood, shop at local markets, use public transit, visit hospitals, and attend expat meetups.

You’re not on vacation; you’re testing a potential life.

Pay attention to how you feel on a Tuesday afternoon, not just on a sunny Saturday morning.

Legal preparation involves your visa application, but also less obvious tasks: setting up a power of attorney for someone back home, ensuring your will is valid across jurisdictions, and understanding tax obligations in both your home country and your destination.

U.S. citizens are taxed on worldwide income regardless of where they live, so you’ll still file with the IRS. Tax treaties between the U.S. and your destination country may prevent double taxation, but the specifics vary.

The emotional dimension is real and often underestimated.

Leaving your existing social network, your familiar routines, and your cultural context is a significant psychological transition.

The Hero Retirement framework addresses this through its four pillars: Health, Enjoyment, Returns, and Opportunity. A successful retirement abroad isn’t just about financial returns or healthcare access. It requires building new sources of enjoyment and pursuing opportunities for growth and connection in your new home.

Managing International Social Security Payments

If Social Security is a significant portion of your retirement income, you need to understand how payments work abroad.

The good news: Social Security can be direct-deposited into bank accounts in most countries. The SSA’s international direct deposit program covers all five countries discussed in this guide.

You’ll want to set up your payments to go directly to a local bank account in your destination country.

This avoids the fees and delays associated with receiving checks by mail. However, keep a U.S. bank account active as well. Some bills, subscriptions, and financial accounts will still require a U.S.-based account, and having one gives you flexibility.

The SSA requires periodic proof that you’re still alive and eligible for benefits.

If you’re living abroad, you may need to visit a U.S. embassy or consulate to complete a “proof of life” questionnaire, or you may receive a form by mail that must be returned. Missing this step can result in suspended payments, so mark your calendar.

Currency conversion is an ongoing cost.

When your Social Security dollars are converted to euros, colones, or ringgit, the exchange rate and any bank fees reduce the actual amount you receive. Services like Wise (formerly TransferWise) or OFX typically offer better exchange rates and lower fees than traditional banks. The difference can save you $50 to $150 per month compared to standard bank transfers, which adds up to $600 to $1,800 per year.

For 2026, the Social Security cost-of-living adjustment (COLA) was 2.8%, bringing the average retired worker benefit to approximately $2,040 per month. If you’re a couple both receiving benefits, your combined income may be $3,500 to $4,500 per month, which provides a comfortable lifestyle in any of the five cities listed here.

Final Checklist for Evaluating Quality of Life Scores

Before committing to a city, run through a structured evaluation. Quality of life is subjective, but you can make it more concrete by scoring each destination across specific categories.

- Healthcare access: Rate the city’s hospital quality, English-speaking medical staff, insurance costs, and emergency response. Weight this category heavily if you have existing health conditions.

- Financial sustainability: Calculate your total monthly budget including rent, food, insurance, transportation, entertainment, and a contingency fund. Compare this to your projected income from Social Security, pensions, and investments. Aim for your income to exceed expenses by at least 15-20%.

- Social connectivity: Assess the size and activity level of the expat community, the availability of clubs and organizations, and the friendliness of the local population toward foreigners.

- Safety and stability: Check the Global Peace Index ranking, local crime statistics, and political stability indicators. Talk to current expat residents about their day-to-day experience.

- Climate and environment: Be honest about your weather preferences. A city that looks perfect on paper won’t work if you’re miserable in tropical humidity or chilly mountain evenings.

- Bureaucratic ease: Evaluate the visa process, residency renewal requirements, and the general efficiency of government services. Some countries make this painless; others test your patience.

Score each category on a 1-10 scale and weight them according to your personal priorities.

A retiree with diabetes will weight healthcare differently than a healthy 60-year-old. Someone with a $4,000 monthly pension has different financial constraints than someone living on $1,800 in Social Security.

Don’t skip the trial period.

Even after all your research, the only way to know if a city works for you is to live there temporarily. Most visa programs allow tourist stays of 30-90 days, which gives you enough time for a meaningful test run.

Your Next Chapter Starts with a Single Step

The best cities for retirement in 2026 share common traits: affordable living costs, accessible healthcare, welcoming communities, and enough cultural richness to keep life interesting.

Whether you’re drawn to Lisbon’s cobblestone charm, Cuenca’s dollar-denominated affordability, or Valencia’s Mediterranean balance, the key is matching a city’s strengths to your specific needs and priorities.

Don’t let the complexity of an international move paralyze you.

Break the process into manageable steps: research, visit, plan, execute.

Thousands of retirees have made this transition successfully, and the infrastructure supporting expat retirement has never been stronger. Your retirement story doesn’t have to be defined by rising costs and shrinking options at home. It can be defined by curiosity, adventure, and the deliberate choice to live well on your own terms.

Frequently Asked Questions

Can I still receive Medicare benefits if I retire abroad?

No. Medicare does not provide coverage outside the United States, with very limited exceptions near the Canadian and Mexican borders. If you retire abroad, you’ll need private health insurance in your destination country, and possibly enrollment in the local public healthcare system if available. Many retirees keep their Medicare Part A (which is premium-free if you’ve paid into the system for 10+ years) active so they have coverage when visiting the U.S., but they rely entirely on local insurance for day-to-day care abroad.

How do taxes work if I’m a U.S. citizen living overseas?

U.S. citizens must file federal income tax returns regardless of where they live. You’re taxed on worldwide income, including Social Security benefits, pension distributions, and investment earnings. However, tax treaties between the U.S. and many countries prevent double taxation on the same income. The Foreign Earned Income Exclusion applies to earned income but not to pensions or Social Security. You should work with a tax professional experienced in expat taxation to structure your withdrawals and income sources efficiently.

What happens to my Social Security if I move to one of these countries?

Social Security payments continue for U.S. citizens living in all five countries listed in this article. Payments can be direct-deposited into a foreign bank account. The SSA may periodically require proof that you’re alive and eligible, typically through a questionnaire or embassy visit. Your benefit amount isn’t reduced because you live abroad, though the COLA adjustments are based on U.S. inflation, not your destination country’s cost of living.

Is it safe to move abroad alone as a retiree?

Safety varies by city, but all five destinations in this guide have established expat communities and relatively low crime rates. Solo retirees should prioritize cities with active social networks, good public transit, and accessible healthcare. Joining expat groups before you move, through Facebook communities, InterNations, or destination-specific forums, helps you build a social foundation before arrival. Loneliness is a bigger risk than physical safety for most solo retirees abroad, so proactive social planning is essential.

How much money do I really need saved before retiring abroad?

Beyond your monthly income from Social Security or pensions, you should have an emergency fund covering at least six to twelve months of expenses in a liquid, accessible account. This buffer protects you against unexpected costs like medical emergencies, currency fluctuations, or the need to return home quickly. For the cities in this guide, that means having $10,000 to $30,000 in accessible savings on top of your regular income stream. If your monthly income comfortably exceeds your projected expenses by 15-20%, you’re in a strong position to make the move.