A 401(k) is one of the most powerful tools you have to build long-term wealth. Yet many people either underutilize it, misunderstand the rules, or miss out on opportunities that could dramatically increase their retirement savings.

If you’ve ever wondered how much you should contribute, whether a Roth or traditional 401(k) is right for you, or how to avoid mistakes like missing your employer match, you’re in the right place. This guide breaks down the most effective 401(k) contribution strategies in plain English — giving you the clarity and confidence to optimize your retirement plan.

The key? Small, consistent decisions today can translate into hundreds of thousands of dollars tomorrow.

Article Highlights

- 2025 contribution limits: You can contribute up to $23,000 if you’re under 50, or $30,500 if you’re 50 or older.

- Employer match = free money. Always contribute at least enough to capture the full match.

- Roth vs Traditional: Roth 401(k) contributions grow tax-free, while traditional contributions grow tax-deferred.

- Catch-up contributions: People aged 50+ can boost savings significantly.

- Asset allocation & rebalancing: Properly diversifying and adjusting investments helps secure long-term growth.

Why 401(k) Contributions Matter

Tax Advantages

One of the biggest reasons to prioritize 401(k) contributions is the tax benefit. With a traditional 401(k), contributions are made pre-tax, which lowers your taxable income today. This can result in a smaller tax bill while allowing more money to compound over time.

A Roth 401(k), on the other hand, doesn’t give you the immediate tax break — but withdrawals in retirement are completely tax-free. This flexibility lets you choose a strategy based on whether you prefer tax savings now or in the future.

Compounding Growth

Compounding is where the real magic happens. Each dollar you contribute earns returns, and those returns themselves start earning returns. Over decades, this snowball effect can multiply your retirement savings dramatically.

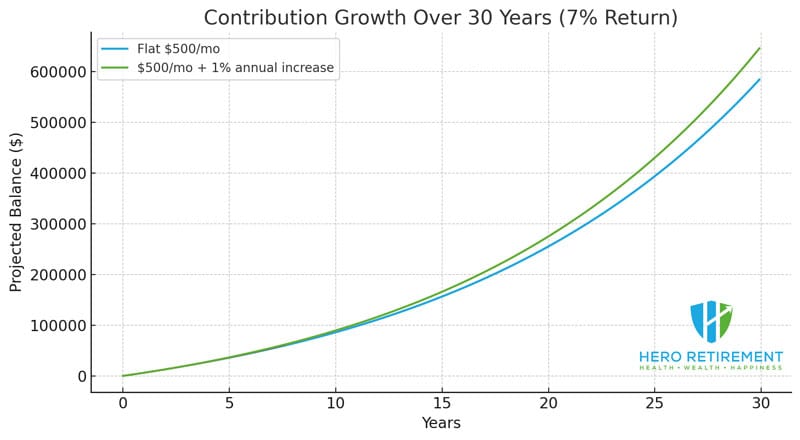

For example: If you invest $500 a month for 30 years and earn an average 7% annual return, you’ll end up with nearly $610,000. That’s the power of starting early and staying consistent.

Understanding 401(k) Contribution Limits for 2025

Standard Limits

For 2025, the IRS allows you to contribute up to $23,000 if you’re under age 50. This is an increase from prior years, reflecting inflation adjustments.

Employers may also contribute through matches or profit-sharing, meaning your total annual 401(k) balance can grow much faster than your contributions alone.

Catch-Up Contributions

If you’re 50 or older, you’re eligible for an additional $7,500 in catch-up contributions. That means your total limit jumps to $30,500 in 2025.

This is crucial for late starters who want to accelerate their retirement savings. Even adding an extra $500 per month for a decade can boost your balance by six figures.

Maximize Employer Match

How Matching Works

Many companies offer a 401(k) match — for example, contributing 50 cents for every dollar you put in, up to 6% of your salary. This is essentially free money added to your retirement account.

Failing to contribute enough to secure the full match is like walking away from a guaranteed bonus.

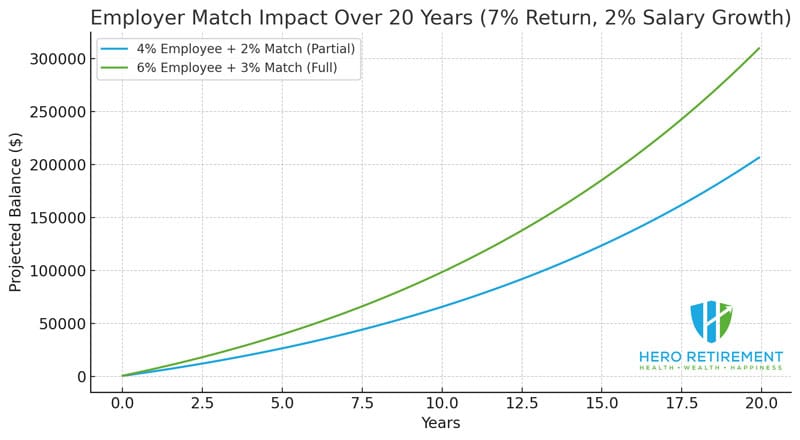

Example of Missed Match Losses

Let’s say you earn $70,000 and your employer matches 50% up to 6%. That’s an extra $2,100 per year if you contribute at least $4,200.

If you skip that match for 20 years, assuming 7% annual growth, you could lose out on over $90,000 in free retirement savings.

Roth vs Traditional 401(k)

Tax Treatment

- Traditional 401(k): Contributions are pre-tax. You lower your taxable income now, but withdrawals in retirement are taxed.

- Roth 401(k): Contributions are after-tax. You don’t get the deduction now, but withdrawals (including earnings) are tax-free.

Which Is Best for You?

It depends on your situation:

- If you expect to be in a lower tax bracket in retirement, a traditional 401(k) often makes sense.

- If you expect to be in a higher tax bracket later, a Roth 401(k) can be more advantageous.

- Many people hedge by splitting contributions between both.

| Feature | Traditional 401(k) | Roth 401(k) |

|---|---|---|

| Payroll Contributions | Pre-tax (lowers taxable income now) | After-tax (no deduction now) |

| Tax on Growth | Tax-deferred (no taxes while invested) | Tax-free growth (qualified withdrawals) |

| Taxes at Withdrawal | Ordinary income taxes on all withdrawals | $0 taxes on qualified withdrawals (age 59½ + 5-year rule) |

| Required Minimum Distributions (RMDs) | Yes, starting at the statutory RMD age | No RMDs on Roth 401(k) balances (current law); rolling to a Roth IRA also avoids RMDs |

| Income Limits to Contribute | None for employee deferrals | None for employee deferrals |

| Early Withdrawal Rules | Taxes + 10% penalty before 59½ (exceptions apply) | Contributions are after-tax; earnings tax/penalty-free only if qualified (59½ + 5-year rule) |

| Best For | Those expecting a lower tax bracket in retirement; want immediate tax break | Those expecting same/higher future tax rate; value tax-free retirement income |

| Key Considerations | Reduces current taxes but creates taxable income later | No deduction now; powerful for long time horizons and tax diversification |

Increase Contributions Over Time

Annual Increase Strategies

Even if you can’t max out your 401(k) right away, commit to gradual increases. A common tactic is to raise contributions by 1% each year, especially when you get a raise.

Over time, these small increments have a massive impact without drastically cutting into your current lifestyle.

Lump Sum vs Monthly Contributions

Dollar-cost averaging — contributing regularly with each paycheck — helps smooth out market volatility. However, if you have a windfall (like a bonus), making a lump-sum contribution early in the year allows more time for compounding.

Optimize Asset Allocation

Stocks, Bonds, and Target-Date Funds

How you invest within your 401(k) matters as much as how much you contribute.

- Younger investors typically benefit from a higher allocation to stocks, which carry higher risk but greater long-term returns.

- Older investors may shift toward bonds and conservative funds for stability.

- Target-date funds automatically adjust your mix as you approach retirement.

Rebalancing Tactics

Rebalancing means realigning your portfolio to your desired mix. For example, if stocks outperform and grow to 80% of your portfolio when your target is 70%, you’d sell some stocks and reinvest in bonds.

Doing this annually or semi-annually prevents your risk profile from drifting out of balance.

Advanced Contribution Strategies

Front-Loading Contributions

Some investors prefer to “front-load” their 401(k) — contributing as much as possible early in the year. This maximizes compounding but requires budgeting discipline.

Be mindful, though: If you max out too early, you may miss part of your employer match (since many match per paycheck).

Mega Backdoor Roth via 401(k)

For high earners, some employers allow after-tax contributions beyond the standard limits. These can be rolled into a Roth IRA through what’s known as a Mega Backdoor Roth strategy.

This tactic can add tens of thousands of dollars per year in Roth savings, but it requires a plan that specifically allows after-tax contributions and in-service withdrawals.

Common 401(k) Mistakes to Avoid

Over-Contributing

If you accidentally exceed the annual limit, you could face IRS penalties. Always track contributions, especially if you change jobs mid-year.

Ignoring Fees

High expense ratios or hidden plan fees can erode your returns over time. Always review your plan’s investment options and opt for low-cost index funds where possible.

Not Rebalancing

Markets shift constantly. Failing to rebalance can leave you either too exposed to risk or too conservative, both of which may harm your long-term goals.

How to Coordinate 401(k) with Other Accounts

IRA Contributions

You can contribute to both a 401(k) and an IRA, subject to income limits. Combining the two gives you flexibility, especially if you want to diversify tax treatment with both Roth and traditional accounts.

HSA Retirement Benefits

If you have a Health Savings Account (HSA), it can double as a stealth retirement account. Contributions are tax-deductible, grow tax-free, and withdrawals for medical expenses are tax-free. After age 65, you can also use HSA funds for non-medical expenses (taxed like a traditional IRA).

Conclusion

Maximizing your 401(k) isn’t about making one big decision. It’s about consistent, strategic moves: contributing enough to get the match, increasing contributions over time, choosing the right tax structure, and managing your investments wisely.

Whether you’re just starting out or fine-tuning your strategy, the choices you make today can define your financial freedom tomorrow.

Take action now: log into your account, check your current contribution rate, and make sure you’re on track to reach your goals. Even a 1% increase today can snowball into life-changing results over decades.

FAQs

What percentage should I contribute to my 401(k)?

A good starting point is 10–15% of your income, including employer match. If that’s not realistic right away, start lower and increase annually.

Can I max out both a 401(k) and IRA?

Yes. In 2025, you can contribute $23,000 (or $30,500 if 50+) to a 401(k) and $7,000 (or $8,000 if 50+) to an IRA, assuming you meet income eligibility rules.

Is a Roth 401(k) better than a traditional 401(k)?

Neither is universally “better.” Roth offers tax-free withdrawals later, while traditional offers tax savings now. Many people use both to hedge against future tax uncertainty.

How do I change my 401(k) contribution rate?

Most employers allow you to adjust your contribution rate anytime through your HR portal or benefits provider. Log in, update your percentage, and the change should take effect in the next payroll cycle.